How to make a chart of accounts?

What is a chart of accounts?

The chart of accounts is a device that lists all the financial accounts in a company’s financial statements and categorizes all financial transactions occurring in a specific period.

Businesses use the chart of accounts to establish their records by offering a complete list of all the accounts in the business’s general ledger. The chart makes it easy to create information for evaluating the company’s financial performance at any given time.

To make a chart of accounts, you’ll need to prepare appropriate account classifications to assign a four-digit enumeration method to the accounts you construct. While making a chart of accounts can be time-consuming, it’s essential for understanding your business’s financial health.

https://youtu.be/U1CQtg_ji_4

What Is a Chart of Accounts?

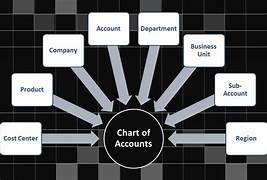

A business’s chart of accounts is a simple list of its financial accounts that becomes a blueprint or roadmap reflecting the business’s economic architecture.

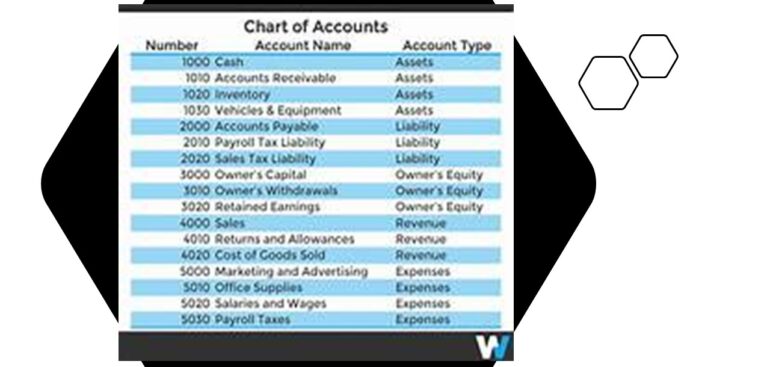

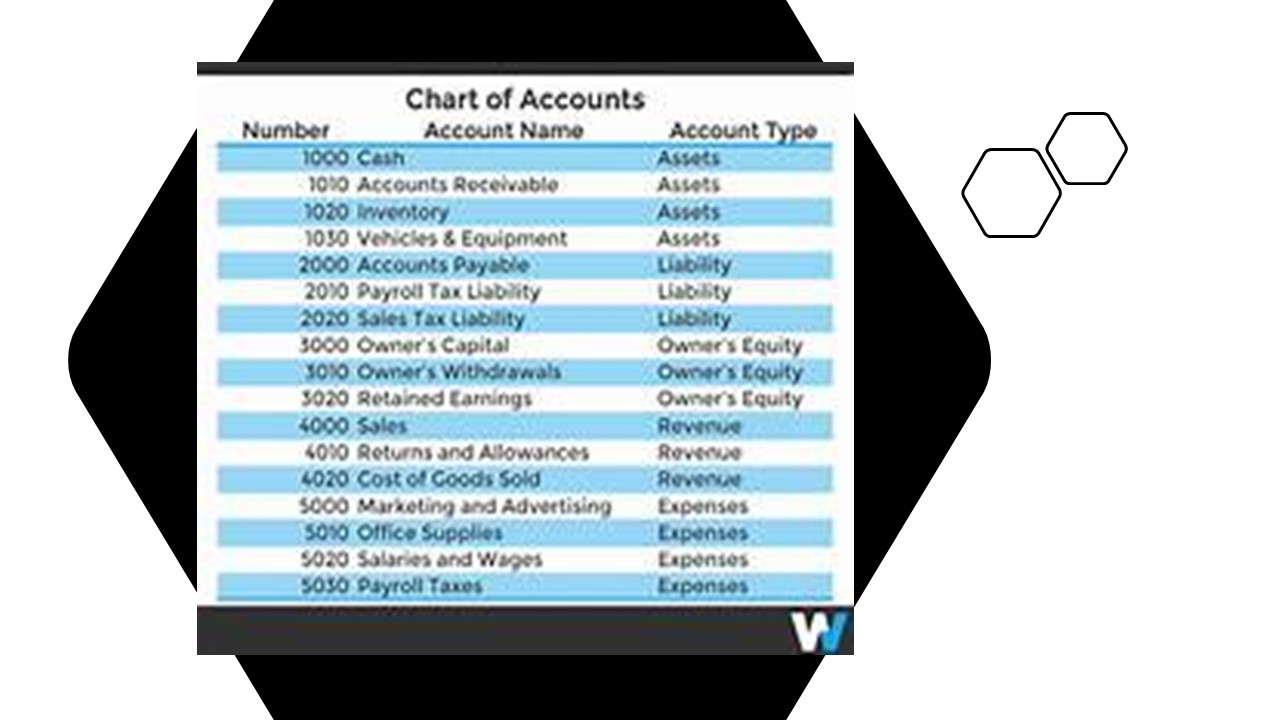

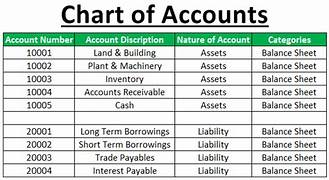

Every account in the chart of accounts relates to the two main financial reports, the balance sheet and the income statement. These accounts are required when preparing a balance sheet for the business. Balance sheet accounts comprise the following:

1. Asset accounts.

A well-constructed chart of accounts enables management to obtain a bird’s-eye view of the company’s financial performance from its general ledger. It also helps the company simplify and streamline end-of-period reporting.

A list of all the monetary accounts included in the financial statements of a company

The chart of accounts provides the name, brief description, and identification codes for each account listed. The balance sheet documents are listed first, followed by the accounts in the profit and loss account.

The balance sheet accounts contain assets, liabilities, and shareholders’ equity, which are further divided into subcategories. The income statement accounts comprise revenues and expenses, which are also further divided into subcategories.

Setting Up the Chart of Accounts

When setting up a chart of accounts, the listed accounts refer to the type of industry. Still, an inventory account will be left out since a teaching business is a service business that does not hold stock.

Naturally, when registering accounts in the chart of accounts, you should use an enumeration method for easy detection. Totaling also makes it easy to record an operation. Small businesses frequently use three-digit numbers, while large companies use four-digit numbers to allow room for additional numbers as the company grows.

Clusters of numbers are allocated to each of the five main classifications, while empty numbers are left at the end to allow surplus accounts to be totaled. The enumeration should also be constant to make it easier for the administration to roll up information about the company from one period to the next.

Example: An extensive business numbering system

Categories on the Chart of Accounts

The chart of accounts shows each account after the two main financial reports, the balance sheet and the income statement.

Balance sheet accounts

Such accounts are required when making a balance sheet for the company. Balance sheet accounts contain the following:

1. Resource accounts

The asset account gives a list of all the classifications of assets that the business owns. The account may include non-physical assets (such as trademarks, patents, and software), current assets (such as cash on hand, accounts receivable, and

Each asset account can be represented in a series such as 1000, 1020, 1040, 1060, etc. The enumeration follows the conventional

balance sheet format, starting with the current and fixed assets.

2. Legal responsibility accounts

Liability accounts present a list of classifications for all the obligations the business owes its creditors. Naturally, obligation accounts will incorporate the word “payable” in their name and may contain accounts payable, invoices payable, salaries payable, interest payable, etc.

Liability accounts follow the traditional balance sheet format, starting with current and long-term liabilities. Long-term liabilities. The numeral arrangement for each charge account can begin in 2000, and an arrangement that is easy to follow and balances in different accounting periods can be used.

3. Owner’s impartiality accounts

Equity signifies the value left in the business after deducting all liabilities from the assets. Owner’s equity represents the company’s value to its investors.

Some owners’ equity accounts incorporate corporate stock, preferred stock, and retained earnings. A large company’s owner’s equity account numbering system can remain from the accountability accounts, from 3000 to 3999.

Income report accounts

The main elements of the income statement accounts include revenue and expense accounts.

1. Revenue accounts

Revenue accounts capture and record the business’s income from selling its products and services. They only include revenues related to the business’s core functions and exclude revenues unrelated to its primary activities.

Some of the subcategories that may be contained under the income account include sales discounts account, sales returns account, interest income account, etc. The enumeration for every income account can begin at 4000.

2. Expense accounts

The expense account is the last classification in the chart of accounts. It consists of a list of all the accounts used to capture the money spent, creating income for the enterprise. The spending can be tied back to specific products or business revenue-generating activities.

An easy way to set up the spending accounts is to make an account for each expense listed on the IRS Tax Form Schedule C and add other accounts specific to the business’s nature. Each expense account can be assigned a number starting from 5000.