How to Save Right for Retirement

Saving should start ASAP

Do not ever postpone. Do not ever think, “When will I get the raise?” Start today. The benefit you get when you start straightaway will grow faster because of compound interest.

It is always better to start saving for retirement; the earlier you begin, the better. When you pay money into a pension, you benefit from tax relief. If you’re a basic-rate taxpayer, a £100 contribution is boosted to £125. Thanks to tax relief and increased investment, any contributions you make today will likely be worth much more when you retire.

https://youtu.be/iuH5vqDOzbI

How much should I save for retirement?

A general rule of thumb is to keep 15% of your annual pre-tax income. This level works best if you consistently save between the ages of 27 and 66. When you start saving for retirement late in life, you may have to rearrange these figures and put a little more to match that standard.

How do I save for retirement?

Do everything feasible not to cash out your retirement funds earlier than usual.

Plunging into your retirement funds early will harm you many times over. First, you’re denying all the hard work you’ve done so far saving—and you’re avoiding spending that money.

Second, you’ll be punished for early leaving, and those penalties are usually hefty. Finally, you’ll get hit with a tax bill for the money you take out. All these reasons make early withdrawal a very last solution.

Give cash to Get cash.

The famous 401(k) ties are when your boss finds your stepping-down account. But you’ll only receive that payment if you make your payment first. That’s why it’s called a tie, see?

When you get an increase, your retirement savings will increase, too.

Do you know how you’ve always told yourself you would save more when you have more? We’re calling you out on that. Every time you get a bump in pay, you should first up your involuntary transfer to funds and enhance your retirement funds. It’s just one step in our checklist for saving for retirement.

How much income should I aim for in retirement?

Saving as much as possible, as early as possible, into your private pensions will help put you in the most vital financial position for life after work. But it’s hard to know exactly how much you should aim for.

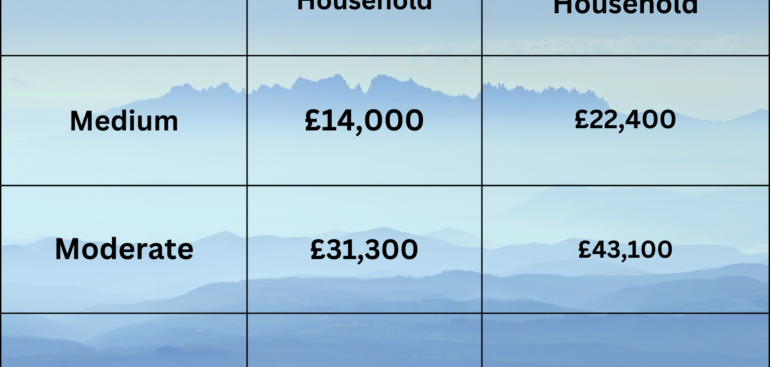

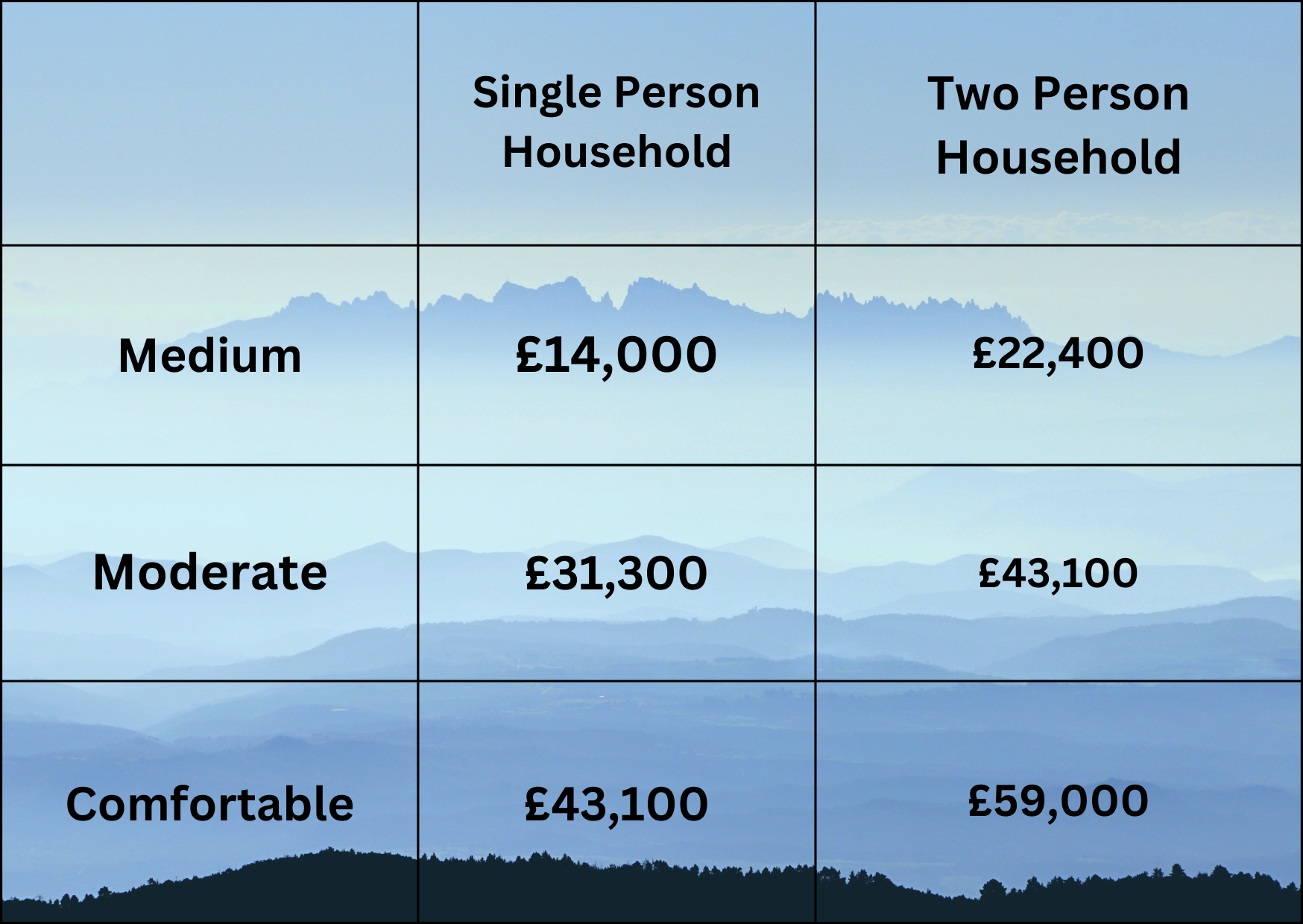

The Pension and Lifetime Savings Association (PLSA) has developed three ‘retirement living standards’ to help address this problem. These reflect the amounts you’d need for a minimum, moderate, and comfortable way of living in retirement:

Source: PLSA retirement living standards. The figures shown reflect the annual expenditure required to achieve each standard.

Source: PLSA retirement living standards. The figures shown reflect the annual expenditure required to achieve each standard.The targets for a person living alone might seem higher than those for couples, but this reflects that many costs – such as energy bills, broadband, and home insurance – are virtually the same even if you live alone.

How far will my retirement income stretch?

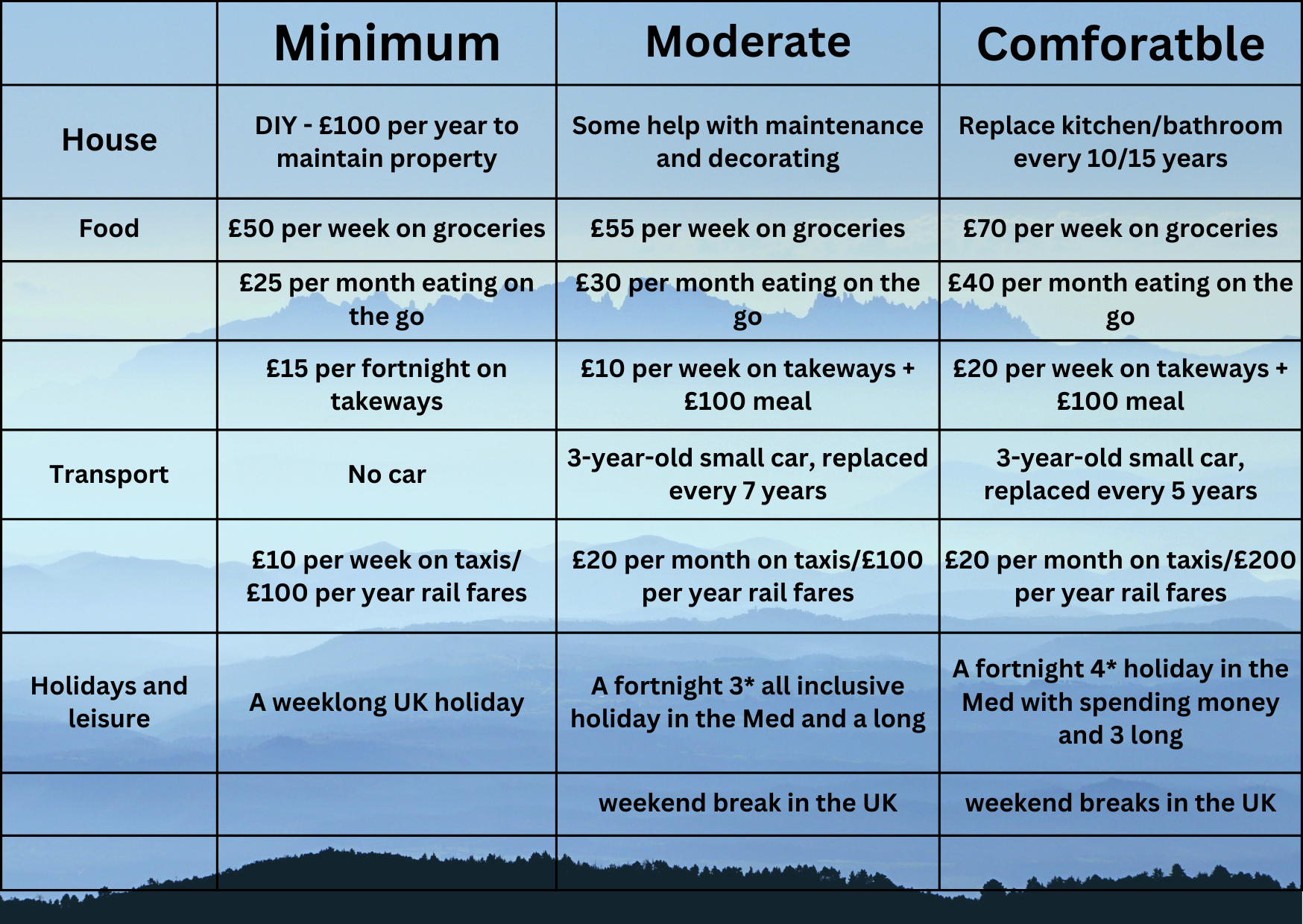

Each PLSA’s three retirement living standards depend on the cost of a basket of goods and services.

Here’s a typical budget for a single retiree aiming for each of the standards across six spending categories:

Source: PLSA

Source: PLSAWhere will my retirement income come from?

A combination of the state pension and private pensions are the building blocks of most people’s retirement income.

State pension

You’ll qualify for payments when you reach 66, but this is scheduled to rise to 67 between 2026 and 2028.

In 2024-25, the whole level of new state pension (for people who reach state retirement pension time on or after 6 April 2016) is £221.20 a week (£11,502.40 a year), but not everyone gets that much. Please find out more in our guide to how much state pension I will get.

Final salary pension

If you have a last salary (defined benefit) pension, you’ll receive a guaranteed income, calculated based on your service length and earnings while working. Deduct tax, and you should know how close you are to your target amount.

You should receive annual updates telling you how much you can expect to get.

Defined contribution pension

Outlined payment pensions are the most usual type of personal pension. You (and your employer, if it’s a workplace scheme) pay them money, which is then invested.

The amount you get when you retire depends on how much you’ve contributed, how well the investments have performed, and how you decide to access your pot

.

Your options for accessing this money are:

• Buying an annuity, which guarantees an income each year for life

• Pension drawdown, where you leave your pension invested and take income as you need it

• Taking lump sums

With HUB Financial Solutions, you can compare annuity options across the market and make the best choice for you.

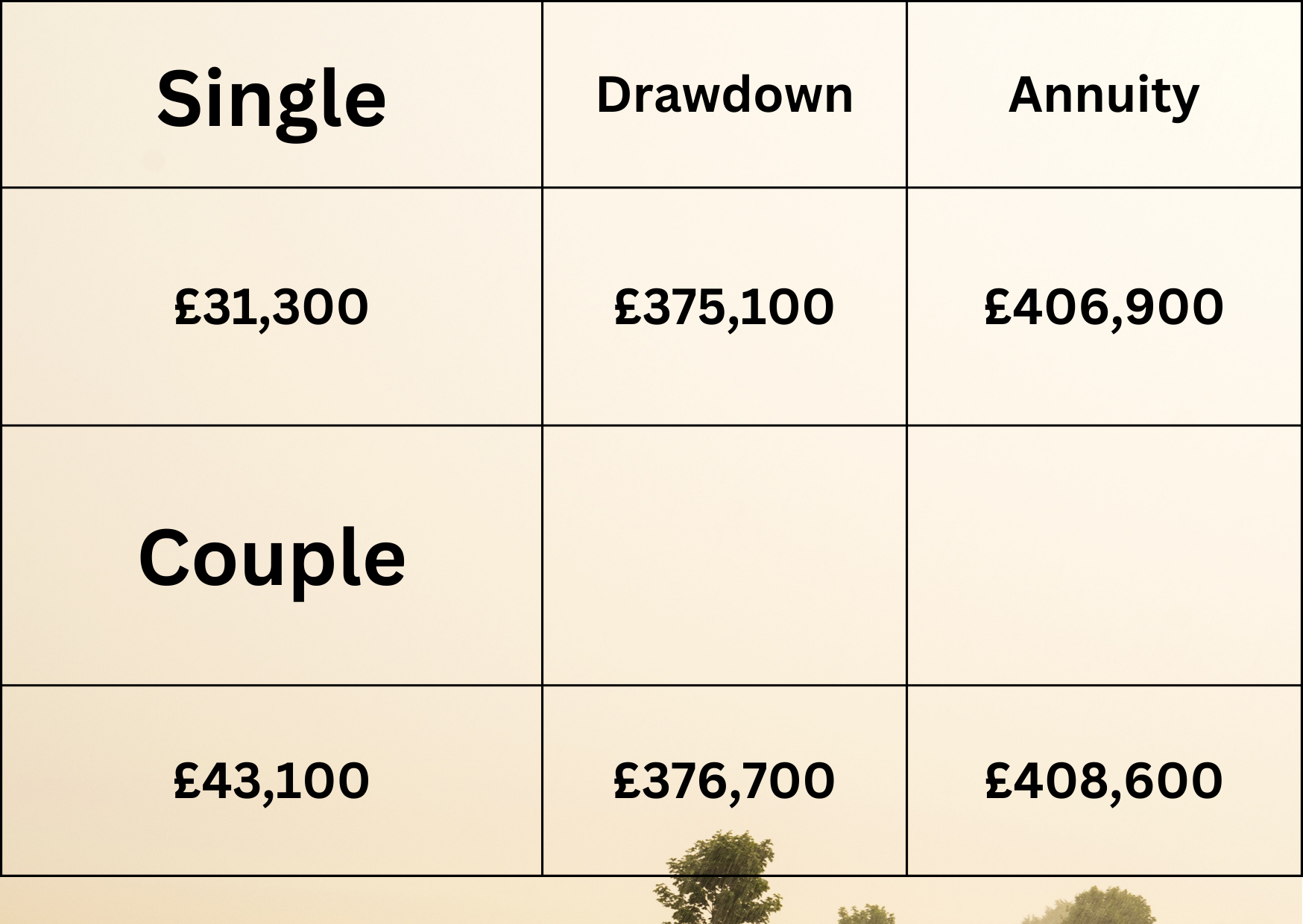

How much do I need to save to reach my target retirement income?

The PLSA’s retirement living standards are designed to give you a better idea of how much you might need to spend each year in retirement. The next step is working out how much you’ll need to save in your pension to generate the gross (before tax) annual income you want.

Retirees living alone face a more formidable challenge, given their higher relative expenditure combined with lower state pension and tax-free allowance than a couple. So, singles must produce a relatively bigger pot.

Retirees living alone face a more formidable challenge, given their higher relative expenditure combined with lower state pension and tax-free allowance than a couple. So, singles must produce a relatively bigger pot.Our drawdown amounts are established on a saver drawing all their money over 20 years from age 65.

We assume investment growth at 3%, inflation at 1%, and charges of 0.75%.

Annuities are more expensive than drawdowns because they produce a guaranteed income for life, which might stretch beyond the average 20-year retirement.

If you take out an annuity from using the service from HUB Financial Solutions, which one? We will earn a commission to help fund our not-for-profit mission.